Financial Policy Inquiries 2026: Compliance & Response Guide

The regulatory pressure on financial institutions is no longer static. Each year, oversight becomes more data-driven, more coordinated across jurisdictions, and more focused on emerging risks. For organizations in banking, insurance, fintech, and related sectors, Financial Policy Inquiries are not rare disruptions — they are part of the operating environment.

In 2026, the question is no longer whether your organization will face regulatory scrutiny. The real question is whether you are structurally prepared for it.

This guide outlines how Financial Policy Inquiries are evolving, what types of reviews institutions encounter, and how to build internal capabilities that turn regulatory interaction into a strategic advantage rather than a liability.

What Financial Policy Inquiries Actually Cover

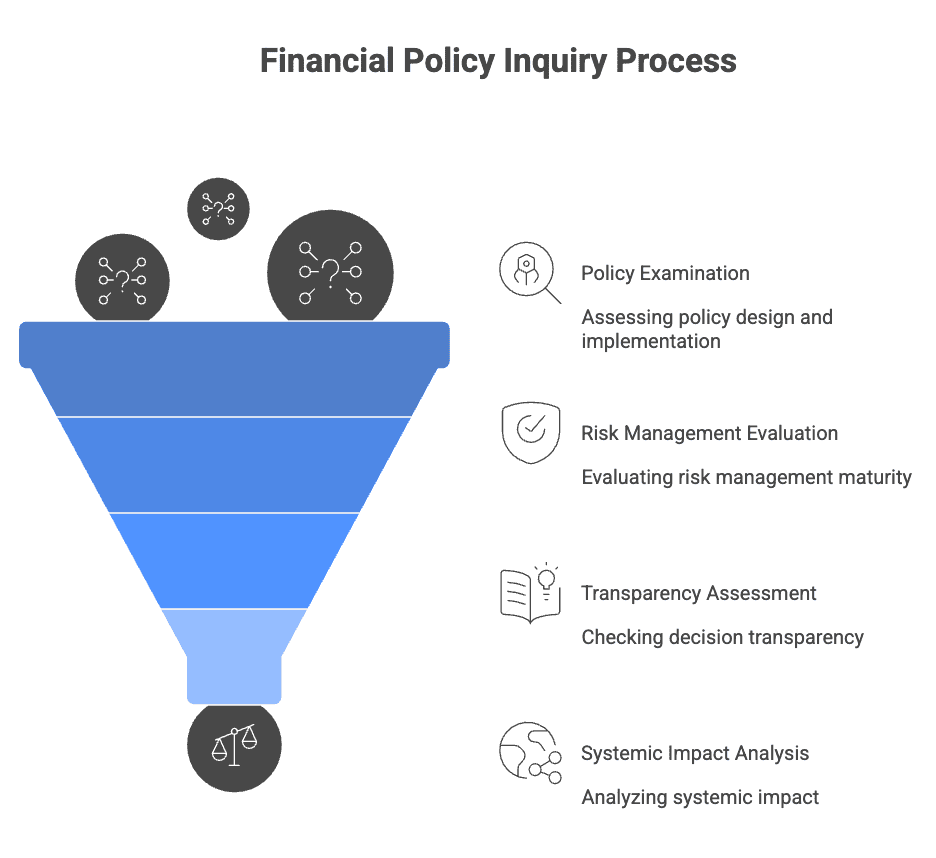

Financial Policy Inquiries are formal examinations, investigations, and regulatory reviews assessing whether institutions comply with applicable financial laws, internal controls, and governance standards.

They typically examine how policies are designed, implemented, monitored, and enforced. Regulators are not only looking for rule adherence — they evaluate risk management maturity, decision transparency, and systemic impact.

These inquiries may be triggered by routine supervisory cycles, data anomalies, customer complaints, whistleblower reports, or broader thematic initiatives. Increasingly, they are informed by advanced analytics that identify patterns long before visible issues surface publicly.

For institutions, these reviews serve two purposes. They can uncover weaknesses and lead to penalties — but they can also validate governance strength and reinforce market credibility when handled effectively.

The Regulatory Shift in 2026: Data, Coordination, and New Risk Areas

The regulatory landscape has shifted in three major ways.

First, oversight is now data-centric. Regulators analyze transaction-level datasets, behavioral trends, and cross-product exposures using increasingly sophisticated tools. Institutions must assume that inconsistencies, outliers, or control gaps are detectable.

Second, cross-border cooperation has intensified. Financial activities operate globally, and supervisory bodies now share intelligence more fluidly. Multi-jurisdiction institutions may find inquiry findings reviewed by several authorities simultaneously.

Third, regulatory focus areas are expanding. Artificial intelligence in credit decisions, digital assets, embedded finance, sustainability disclosures, and climate risk management are drawing growing attention. Regulators are moving quickly to understand and shape these domains, meaning early movers in innovation often face early scrutiny.

Compliance is no longer about checking static boxes. It requires adaptive governance capable of responding to evolving expectations.

Understanding the Types of Inquiries You May Face

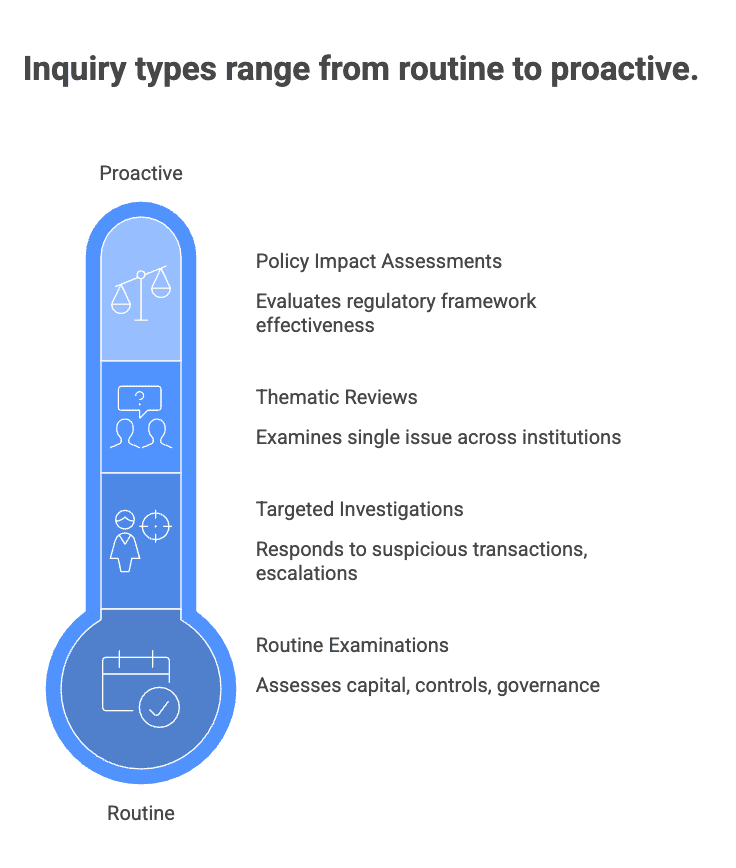

Not all inquiries carry the same implications. Understanding the differences helps institutions calibrate response strategy.

Routine supervisory examinations follow established schedules. These reviews assess capital adequacy, operational controls, governance structures, and compliance programs. They allow preparation but require thorough documentation readiness.

Targeted investigations arise from specific triggers — suspicious transaction reports, customer escalations, or anomalies detected in regulatory monitoring. These inquiries are more urgent and narrower in scope, often requiring rapid mobilization of legal and compliance teams.

Thematic reviews examine a single issue across multiple institutions. Regulators may focus on topics like fee transparency, fair lending practices, cybersecurity preparedness, or AI decision frameworks. These reviews provide insight into sector-wide expectations and emerging enforcement priorities.

Policy impact assessments evaluate whether regulatory frameworks achieve intended outcomes. Institutions participating constructively in these discussions can influence future rulemaking while demonstrating maturity in governance.

Each type requires a distinct but coordinated internal response model.

Building an Inquiry-Ready Organization

The strongest institutions do not scramble when inquiries begin. They operate with inquiry readiness embedded in daily processes.

Clear governance structures are foundational. Designated leaders must oversee regulatory engagement, supported by documented escalation paths and board-level awareness when material issues arise. Regulators evaluate tone from the top as closely as procedural adherence.

Comprehensive documentation is equally critical. Policies, decision rationales, transaction histories, and control logs should be organized, searchable, and aligned with retention standards. Delayed or incomplete documentation signals control weakness, even when underlying compliance exists.

Internal testing and monitoring provide an early warning system. Institutions that proactively identify control gaps and remediate them demonstrate accountability. Regulators consistently respond more favorably to self-identified and corrected issues than to externally discovered failures.

Staff training must extend beyond compliance teams. Business units, operations personnel, and technology functions should understand escalation procedures and communication boundaries during inquiries. Clarity prevents misstatements and inconsistent responses.

Preparation reduces disruption. It also builds credibility.

Strategic Response: What to Do When an Inquiry Begins

When a Financial Policy Inquiry is initiated, initial positioning matters.

A structured assessment should clarify scope, timeline, potential exposure, and whether legal counsel should be engaged. Early understanding prevents overreaction or underestimation of regulatory concern.

Communication strategy is critical. Transparency and cooperation typically produce better outcomes than adversarial posture. However, all responses must remain precise, documented, and within scope. Informal or speculative statements can inadvertently create binding commitments.

Resource allocation should be realistic. Inquiry management often competes with operational priorities. Institutions that dedicate sufficient expertise — including compliance specialists, legal advisors, and data analysts — manage processes more efficiently and avoid regulator frustration.

Cross-functional coordination prevents inconsistencies. Legal, compliance, operations, IT, and executive leadership must align messaging and documentation to ensure coherent responses.

An inquiry is not merely a compliance test. It is a test of institutional coordination and governance resilience.

Remediation and Post-Inquiry Strengthening

Inquiries often conclude with findings requiring corrective action. The quality of remediation frequently determines long-term regulatory relationships.

Effective remediation addresses root causes rather than superficial symptoms. Regulators look for structural improvements, not isolated fixes. Demonstrating systemic strengthening builds supervisory confidence.

Ongoing monitoring verifies remediation effectiveness. Institutions should test corrective measures, evaluate residual risk, and maintain documentation showing sustained improvement.

Post-inquiry internal reviews are equally valuable. Organizations should analyze what worked, what created friction, and how governance or documentation processes can improve.

The most resilient institutions treat inquiries as catalysts for strengthening internal discipline.

Technology’s Expanding Role in Regulatory Engagement

Technology is reshaping both regulatory oversight and institutional response.

Modern data management systems allow rapid retrieval of requested documentation. Fragmented records, by contrast, slow responses and raise concerns.

Advanced analytics tools support proactive compliance by identifying anomalies internally before they attract external scrutiny. The same systems accelerate inquiry responses by enabling structured data extraction and reporting.

Regulatory technology platforms automate reporting, maintain audit trails, and centralize compliance workflows. These capabilities reduce manual error and improve transparency.

Artificial intelligence is emerging as a monitoring tool on both sides. Regulators deploy AI to identify suspicious patterns, while institutions use AI for internal risk detection. Institutions deploying AI in credit, underwriting, or claims processes should expect increased regulatory examination of model governance and bias controls.

Technology enhances readiness — but only when governance frameworks oversee its application.

Preparing for What Comes Next

Regulatory expectations will continue evolving. Institutions should anticipate broader supervisory reach into digital ecosystems, climate risk disclosures, AI governance frameworks, and embedded finance structures.

Data requirements will likely become more granular. Institutions should invest in scalable infrastructure capable of supporting detailed regulatory submissions.

International cooperation will deepen, increasing the likelihood of coordinated reviews across jurisdictions.

Organizations that treat compliance as dynamic rather than static will adapt more effectively.

Conclusion

Financial Policy Inquiries are not exceptional events — they are integral to operating within regulated financial ecosystems. Institutions that prepare strategically, maintain strong governance, leverage technology responsibly, and respond transparently build long-term resilience.

The most successful organizations do not merely survive inquiries. They use them to demonstrate operational integrity, reinforce stakeholder trust, and differentiate themselves in increasingly scrutinized markets.

In 2026 and beyond, inquiry readiness is not optional. It is a defining feature of sustainable financial institutions.

Contact Us

Connect with sourceCode

If you found this message inspiring and wish to stay updated with our expert insights, be sure to Follow sourceCode on LinkedIn today!

Additionally, if you are interested in strategic partnerships, innovative technology solutions, or exciting career opportunities, don't hesitate to visit our official website: sourcecode.com.au