AI Loan Origination for Digital Lending: OCR and Credit Scoring

In the context of rapid digital transformation, the financial services industry is undergoing a fundamental shift in how credit is originated and approved. Traditional lending processes, which rely heavily on manual verification and rigid risk models, are increasingly being replaced by intelligent, automated systems. In this evolving landscape, AI Loan Origination has emerged as a critical solution for streamlining and modernizing the end-to-end lending lifecycle.

At the same time, Credit Scoring for Digital Lending plays a central role in enabling faster and more accurate risk assessment. Supported by large-scale data processing and advanced machine learning techniques, modern credit scoring systems are redefining how financial institutions evaluate borrowers. Optical Character Recognition (OCR), as a foundational technology, facilitates the digitization of input data, allowing AI systems to operate efficiently and at scale.

What Is AI Loan Origination?

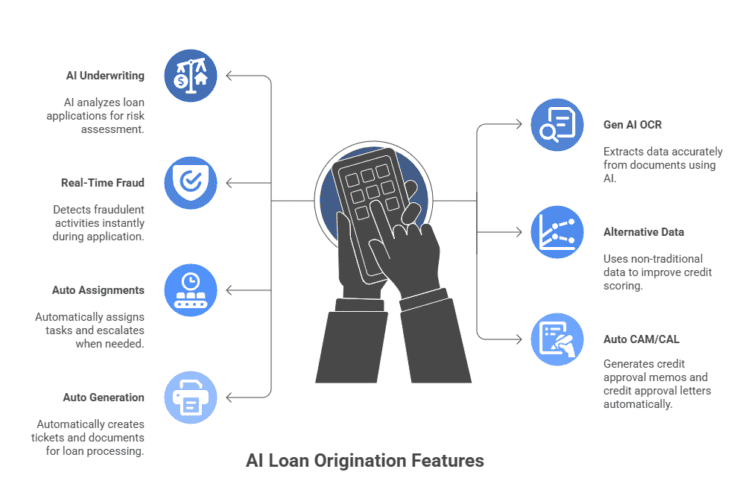

AI Loan Origination refers to the application of artificial intelligence technologies to automate the entire loan initiation process, from application intake and identity verification to risk assessment and approval. Unlike traditional workflows that depend on manual intervention, AI-driven systems can process vast amounts of structured and unstructured data in real time.

According to LoanPro (2026), AI in lending is evolving from a supporting tool into core infrastructure, enabling financial institutions to handle high volumes of applications with increased speed and consistency. This transformation significantly reduces approval times—from several days to just minutes—while also improving operational efficiency and customer experience.

Moreover, AI Loan Origination enhances decision-making by incorporating multiple data sources and predictive analytics. This allows lenders to go beyond conventional credit metrics and adopt a more holistic approach to risk evaluation.

The Role of OCR in Digital Lending

OCR technology enables the extraction and digitization of text from images and physical documents. Within the AI Loan Origination ecosystem, OCR serves as a crucial bridge between raw input data and AI-driven analysis.

By converting documents such as national IDs, bank statements, and utility bills into machine-readable formats, OCR eliminates the need for manual data entry. This not only reduces human error but also accelerates the processing of loan applications. When combined with AI and natural language processing (NLP), OCR systems can interpret context and identify relevant data points with high accuracy.

As digital lending expands across emerging markets, particularly in regions with limited structured data infrastructure, OCR becomes even more essential in enabling scalable and inclusive financial services.

Credit Scoring for Digital Lending

Credit Scoring for Digital Lending involves the use of AI and data analytics to evaluate a borrower’s creditworthiness. Unlike traditional credit scoring models that rely primarily on credit history and income data, modern systems incorporate a wide range of alternative data sources.

AI-based credit scoring models can significantly improve predictive accuracy by leveraging behavioral data, transaction patterns, and non-traditional indicators such as mobile usage or utility payments. This approach not only enhances risk assessment but also expands access to credit for underserved populations, including individuals with limited or no formal credit history.

Furthermore, AI enables dynamic and adaptive scoring models that continuously learn from new data. This allows financial institutions to respond more effectively to changing economic conditions and borrower behavior, making Credit Scoring for Digital Lending a key driver of innovation in fintech.

The Integration of OCR and AI in Loan Origination

The integration of OCR and AI creates a fully automated and seamless loan origination process. When a borrower submits documents, OCR extracts relevant data and feeds it into AI models for analysis. These models then perform risk assessment and generate credit scores, enabling near-instant approval decisions.

According to Lucid (2025), this end-to-end automation significantly improves operational efficiency and reduces reliance on manual processes. By minimizing human intervention, financial institutions can achieve higher accuracy, faster turnaround times, and greater scalability.

This integrated approach is particularly valuable in high-volume lending environments, such as digital banks and fintech platforms, where speed and precision are critical competitive advantages.

Challenges and Risks in 2025–2026

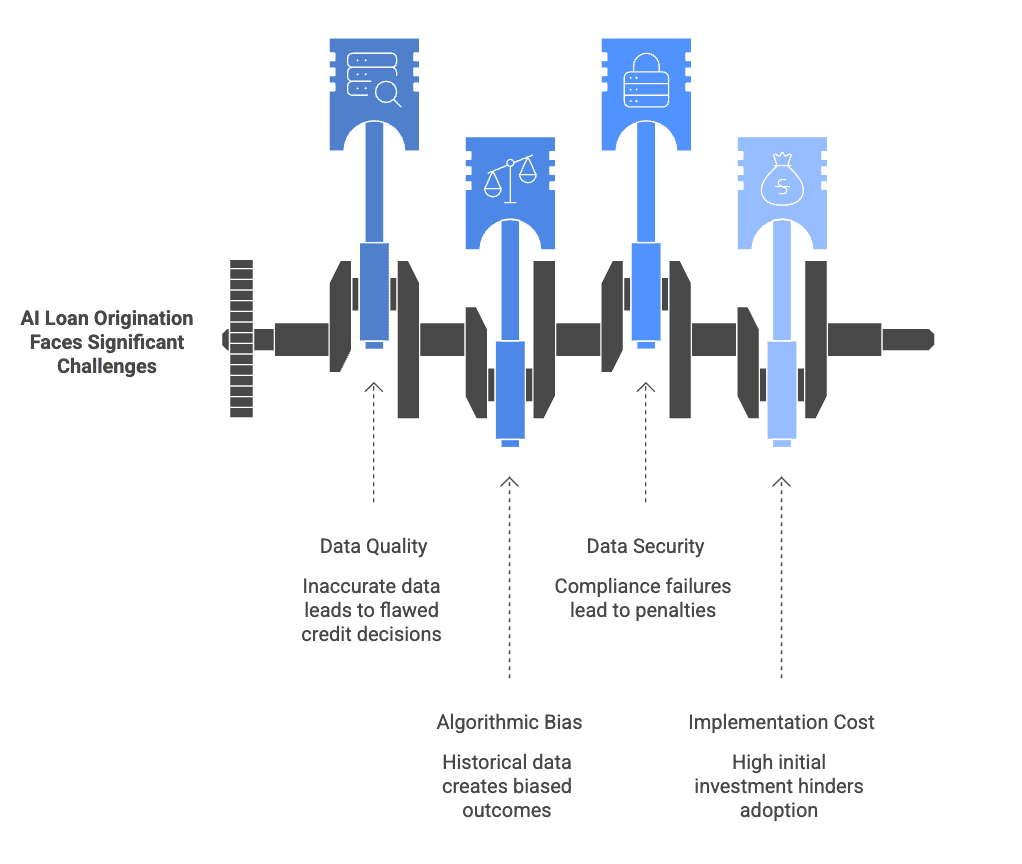

Despite its transformative potential, AI Loan Origination presents several challenges and risks that must be carefully managed, particularly as adoption expands globally and across diverse regulatory environments such as APAC, North America, and Europe.

One of the primary concerns is data quality. AI systems are highly dependent on the accuracy and completeness of input data. According to Appwrk (2025), poor data quality can lead to inaccurate predictions and flawed credit decisions. This issue is especially pronounced in APAC markets, where data fragmentation and inconsistent record-keeping remain significant challenges in some countries.

Another critical issue is algorithmic bias. According to MoFo Tech (2026), AI models may unintentionally produce biased outcomes due to historical data patterns, even when sensitive attributes such as gender or ethnicity are excluded. In regions like the United States and the European Union, regulatory scrutiny around fairness and non-discrimination is intensifying, requiring financial institutions to implement bias mitigation and model auditing frameworks. In APAC, while regulations are still evolving, there is increasing awareness and policy development around ethical AI.

Data security and regulatory compliance also represent major challenges. Financial institutions must comply with a growing number of regulations related to data privacy, explainability, and consumer protection. For example, global standards such as GDPR in Europe and emerging AI governance frameworks in APAC are pushing organizations to ensure transparency in automated decision-making. According to LoanPro (2026), failure to meet these requirements can result in legal penalties and reputational damage.

Finally, the initial cost of implementation remains a barrier, particularly for smaller financial institutions. Building AI infrastructure, integrating with legacy systems, and hiring skilled personnel require substantial investment. However, the rise of cloud-based AI platforms and fintech partnerships is gradually lowering these entry barriers, especially in fast-growing digital economies across Southeast Asia.

Future Trends in 2025–2026

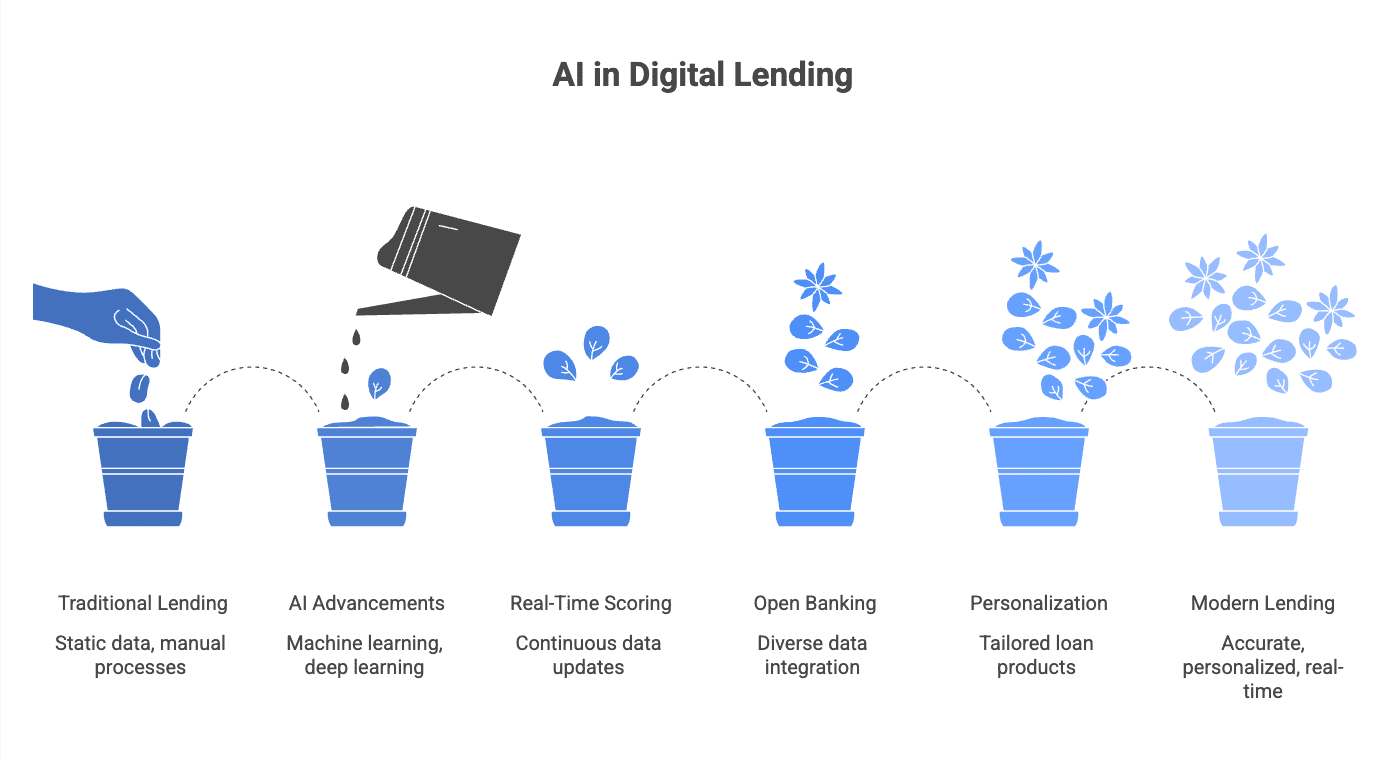

Looking ahead, several key trends are shaping the future of AI Loan Origination and Credit Scoring for Digital Lending, with notable variations across regions such as APAC, North America, and Europe.

First, AI technologies are becoming increasingly sophisticated. According to LoanPro (2026), advancements in machine learning, deep learning, and generative AI are enabling more accurate and adaptive models. In APAC, where fintech innovation is accelerating rapidly, countries such as Singapore and India are leading the adoption of advanced AI-driven lending platforms.

Second, real-time credit scoring is emerging as a standard capability. Instead of relying on static snapshots of borrower data, AI systems can now continuously update credit scores based on real-time inputs. This is particularly relevant in fast-paced digital lending markets, including Southeast Asia, where Buy Now Pay Later (BNPL) services are experiencing rapid growth.

Third, the expansion of open banking and big data ecosystems is transforming access to financial information. According to the American Economic Association (2026), integrating diverse data sources improves risk prediction and reduces default rates. In APAC, open banking initiatives in countries like Australia and Singapore are enabling greater data sharing and fostering innovation in credit scoring.

Finally, personalization is becoming a defining feature of modern lending. AI systems are increasingly capable of tailoring loan products, interest rates, and repayment plans to individual customer profiles. This shift from standardized offerings to personalized financial solutions reflects a broader trend toward customer-centricity in digital finance.

Conclusion

In conclusion, AI Loan Origination is rapidly becoming a foundational component of digital transformation in the financial industry. By integrating OCR and advanced AI technologies, financial institutions can automate the entire lending process, improve decision accuracy, and enhance customer experience.

At the same time, Credit Scoring for Digital Lending enables more inclusive and data-driven risk assessment, expanding access to credit while maintaining control over default risks. However, to fully realize these benefits, organizations must address challenges related to data quality, algorithmic bias, and regulatory compliance.

As AI technologies continue to evolve, they are expected to move beyond operational support and become the central intelligence driving modern lending ecosystems across global and regional markets.

References

- LoanPro. (2026). AI in lending trends.

- MoFo Tech. (2026). AI and algorithmic bias in financial services.

- American Economic Association (AEA). (2026). Big data and credit risk modeling.

Contact Us

Connect with sourceCode

If you found this message inspiring and wish to stay updated with our expert insights, be sure to Follow sourceCode on LinkedIn today!

Additionally, if you are interested in strategic partnerships, innovative technology solutions, or exciting career opportunities, don't hesitate to visit our official website: sourcecode.com.au